A Merchant Cash Advance (MCA) is a type of financing option used primarily by small and medium-sized businesses to gain quick access to capital. Unlike traditional loans, an MCA provides a lump-sum payment in exchange for a percentage of future credit card sales or daily bank deposits. While this form of funding is fast and relatively easy to obtain, it comes with high costs and rigid repayment structures.

Defaulting on an MCA occurs when a business fails to meet the agreed-upon terms of the repayment. This can lead to severe financial, legal, and operational consequences for the borrower. In this article, we’ll explore what it means to default on an MCA, the signs, the aftermath, and how to prevent or handle such a situation strategically.

If you’re already struggling with your Merchant Cash Advance (MCA) and at risk of defaulting—or have already defaulted—there are actionable steps you can take to stop the situation from escalating. The key is to act quickly, strategically, and with transparency, because the longer you delay, the more aggressive the consequences can become.

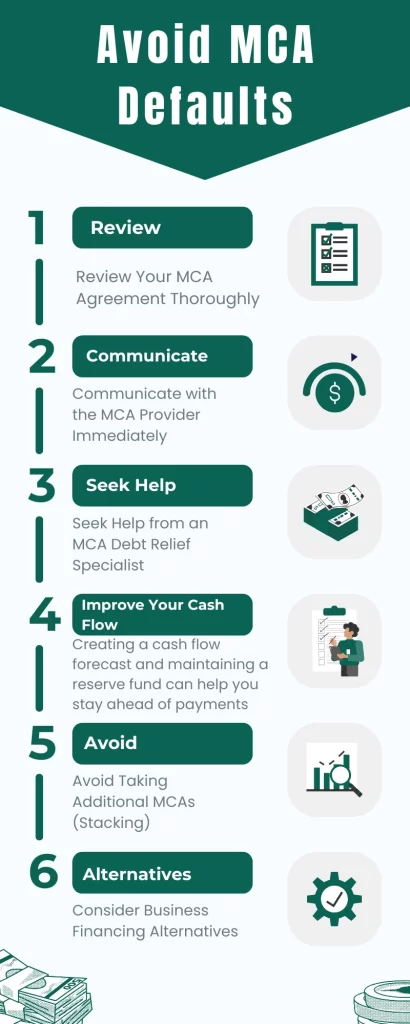

1. Review Your MCA Agreement Thoroughly

Start by carefully reviewing the terms and clauses in your MCA contract. Identify what specifically triggers a default, whether there’s a confession of judgment (COJ), personal guarantee, or daily deduction requirement. Understanding the contract helps you know your rights and the lender’s legal limits. Knowing exactly where you stand will guide your next moves more effectively.

2. Communicate with the MCA Provider Immediately

Reach out to your MCA provider as soon as you know you can’t meet your payment obligations. Many lenders are open to negotiation, especially if they believe you’re acting in good faith. You may be able to restructure the repayment plan, request a temporary reduction in deductions, or agree on a deferred payment schedule. Lenders may prefer restructuring over legal proceedings, which can be costly and time-consuming for both parties.

3. Seek Help from an MCA Debt Relief Specialist

If communication fails or you’re overwhelmed by multiple advances, contact a professional MCA debt relief firm or a qualified attorney. These professionals can negotiate with lenders on your behalf, consolidate multiple MCAs, or even help defend you legally if a COJ or lawsuit has been filed. They can also help you settle the debt for less than what you owe or structure a managed payment plan to stop defaulting.

4. Improve Your Cash Flow Management

Take control of your business’s finances to ensure you can consistently make payments. This may include:

- Cutting non-essential expenses

- Boosting revenue through short-term promotions

- Delaying non-urgent purchases or expansions

- Renegotiating terms with vendors to free up cash

Creating a cash flow forecast and maintaining a reserve fund can help you stay ahead of payments and avoid another default.

5. Avoid Taking Additional MCAs (Stacking)

Many businesses make the mistake of taking out additional MCAs to cover existing ones, a practice known as stacking. This only deepens your financial hole and increases your risk of future default. If you’ve already stacked advances, it’s even more crucial to seek professional assistance to break the cycle and consolidate the debt responsibly.

6. Consider Business Financing Alternatives

Explore lower-risk funding alternatives such as SBA loans, business lines of credit, invoice factoring, or term loans with better interest rates and more flexible repayment terms. These options may be harder to qualify for but offer far more sustainable solutions compared to the high-pressure structure of an MCA.

Taking steps to stop defaulting on an MCA is not just about catching up on payments—it’s about restructuring your business’s financial foundation to ensure long-term stability. Acting early, seeking expert guidance, and making responsible financial decisions are key to breaking free from the MCA trap.