Merchant Cash Advances (MCAs) have gained immense popularity in the world of alternative financing, especially for small to medium-sized businesses seeking fast access to capital. However, the process behind approving an MCA isn’t as instant as it may seem. MCA underwriting is a critical component that determines whether a merchant is eligible for funding, how much they can receive, and under what terms.

This guide dives deep into the underwriting process of MCAs, exploring what it is, how it works, what criteria are considered, and how businesses and funders can optimize the process for better outcomes. Whether you’re a merchant seeking funding or a broker/funder looking to improve your underwriting system, this article covers all aspects.

MCA (Merchant Cash Advance) underwriting offers several advantages for both funders and small business owners seeking fast and flexible financing. One of the primary benefits is the speed of approval; MCA underwriting processes are typically much quicker than traditional loan evaluations, often delivering funding within 24 to 48 hours. This rapid turnaround is ideal for businesses that need immediate capital to cover urgent expenses or seize time-sensitive opportunities.

Additionally, MCA underwriting places less emphasis on credit scores and collateral, focusing instead on the company’s daily or monthly revenue. This makes it accessible to a wider range of businesses, especially those with less-than-perfect credit. Another benefit is the adaptability of repayment structures—repayments are usually based on a percentage of daily sales, aligning the business’s repayment capacity with its cash flow.

As a result, businesses do not face fixed monthly obligations during slower periods. Overall, MCA underwriting provides a streamlined, credit-flexible, and revenue-based solution that empowers small businesses with timely access to working capital.

The MCA (Merchant Cash Advance) underwriting process involves assessing a business’s financial health to determine its eligibility for funding, and the criteria used are different from traditional loans. Since MCA funding is based on future receivables, the underwriting process focuses primarily on a business’s cash flow and ability to repay the advance. Below are the key criteria used during the MCA underwriting process:

1. Business Revenue and Cash Flow

The most critical factor in MCA underwriting is the business’s daily or monthly revenue. Underwriters will request recent bank statements (typically 3-6 months) to analyze:

- Average daily or monthly deposits

- Consistency in revenue (steady income over time vs. seasonal fluctuations)

- Deposit frequency (daily deposits indicate stronger cash flow)

Why it matters: The merchant’s ability to repay the advance is directly tied to their cash flow, so consistent and high revenue is essential.

2. Time in Business

Most MCA providers require that a business has been operating for a minimum amount of time, typically around 3 to 6 months, before they are eligible for an advance. This ensures that the business has a proven track record and a steady revenue stream.

Why it matters: Newer businesses are considered riskier due to limited financial history, and older businesses are typically more stable and predictable in terms of revenue.

3. Industry and Business Type

The type of business and the industry in which it operates also influence the underwriting decision. Certain industries, like restaurants or retail, may be considered higher risk due to their vulnerability to economic fluctuations and seasonality. On the other hand, more stable industries like healthcare or technology may face less risk.

Why it matters: The industry can impact a business’s overall revenue stability and repayment capability. High-risk industries might face stricter lending terms or lower advances.

4. Personal and Business Credit Scores

Although MCA underwriting does not prioritize credit scores as much as traditional loans, some providers will still check both the personal credit of the business owner and the business credit profile (if applicable). A poor credit score can be a red flag, although it may not automatically disqualify a merchant from receiving an advance.

Why it matters: While MCA is more flexible than traditional financing, credit scores can provide additional insight into the merchant’s financial management and payment history.

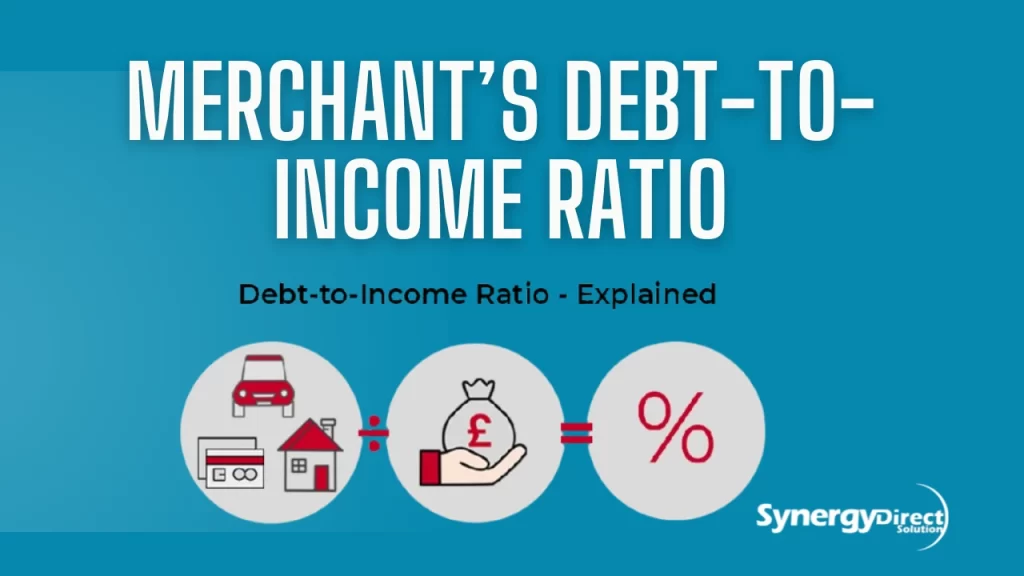

5. Merchant’s Debt-to-Income Ratio

This ratio compares the merchant’s business debts to their income, helping underwriters assess the merchant’s ability to handle additional debt. A high debt-to-income ratio could indicate financial strain, making it riskier for the lender to provide funding.

Why it matters: A lower ratio signifies that the business has sufficient cash flow to handle the new debt without overextending its resources.

6. Chargeback History and Payment Consistency

Underwriters will also examine the merchant’s chargeback history. Frequent chargebacks or refunds could signal issues with product quality, customer service, or business management, all of which can impact the merchant’s future revenue and repayment ability.

Why it matters: A high chargeback rate increases the likelihood of irregular revenue, which affects the merchant’s ability to repay the advance on time.

7. Repayment Structure and Terms

Once all the above criteria are analyzed, underwriters determine the terms of the MCA, including the advance amount, factor rate, and repayment schedule. Repayments are typically tied to a percentage of the merchant’s daily or weekly sales, meaning repayment amounts fluctuate depending on revenue performance.

Why it matters: The repayment structure must be designed to ensure that the business can meet obligations without impacting its daily operations, making a revenue-based repayment schedule more suitable for businesses with fluctuating sales.