In today’s competitive business environment, understanding your financial footprint is critical. Two key tools for evaluating a business’s financial reliability are UCC data and business credit reports. While they may sound similar and even overlap in some areas, they serve distinct purposes and offer unique insights into a company’s creditworthiness and financial obligations.

UCC data—short for Uniform Commercial Code filings—provides detailed records of secured transactions, whereas business credit reports offer a broader overview of a company’s credit history, payment behaviors, and overall financial reputation. Both are essential for lenders, suppliers, and even competitors looking to assess the financial risk associated with doing business with a company.

In this article, we’ll break down the key differences between UCC data and business credit reports, why each is important, and how businesses can use them to make informed decisions.

A business credit report is a critical tool for evaluating a company’s financial reputation and ability to meet its obligations. Just as personal credit reports help lenders assess individual borrowers, business credit reports provide detailed insights into how a company manages debt, pays vendors, and handles credit lines. These reports—issued by bureaus such as Dun & Bradstreet, Experian Business, and Equifax Business—play a vital role in financing decisions, vendor relationships, insurance underwriting, and partnership evaluations.

One of the main reasons business credit reports are important is because they influence access to capital. Lenders use them to determine whether a business qualifies for loans, credit cards, lines of credit, or leasing arrangements. A strong report with timely payments and low credit utilization increases the chances of approval and favorable interest rates, while a poor report may lead to rejections or higher borrowing costs.

In addition, suppliers and vendors often review business credit reports before extending trade credit terms. A positive credit profile can lead to longer payment cycles or larger credit limits, which helps a business improve cash flow and scale operations more effectively. On the flip side, a negative report may force the business to pay upfront or operate on strict terms, limiting financial flexibility.

Another reason business credit reports are valuable is their role in business credibility and trustworthiness. When forming partnerships or bidding on contracts, potential collaborators often review these reports to ensure your company is financially stable. A good credit report enhances your brand’s reputation and can open doors to new opportunities.

Finally, business credit reports help business owners stay informed. By monitoring these reports regularly, companies can detect errors, unauthorized activity, or outdated UCC filings that might otherwise harm their borrowing capacity or public image.

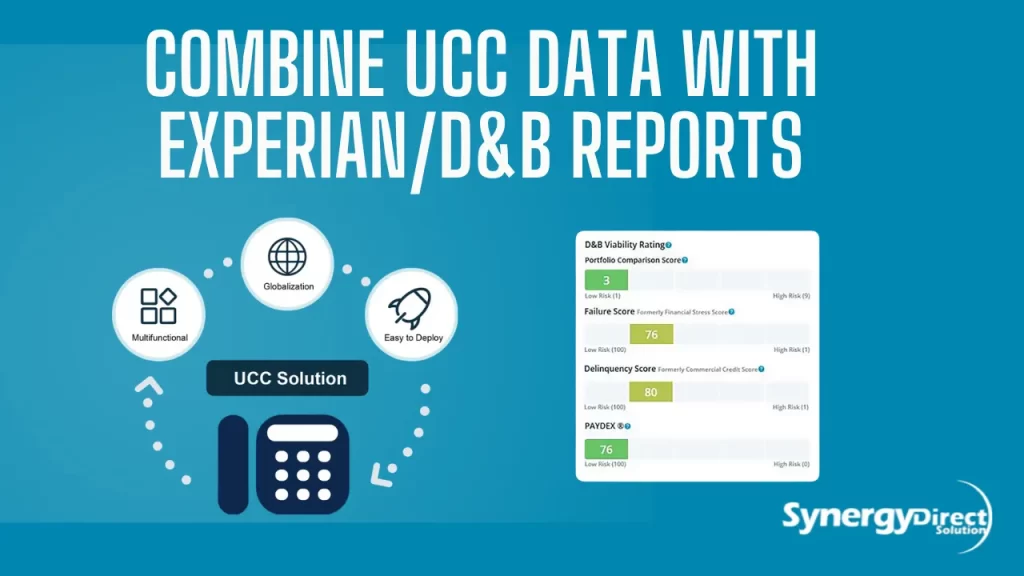

Combining UCC leads data with Experian and Dun & Bradstreet (D&B) business credit reports provides a more comprehensive view of your company’s financial health and borrowing risks. This integrated approach allows you to evaluate not only your credit performance but also your secured debt obligations and collateral exposure, giving lenders and stakeholders a clearer picture of your financial position.

To start, request your business credit reports from both Experian Business and D&B. These reports typically include UCC filing summaries, but they may not always show full details. To access complete UCC data, visit the Secretary of State’s website where your business is registered and download the full UCC-1 filings associated with your business. These filings include essential data like lender names, filing dates, collateral descriptions, and termination statuses.

Once you have both reports and full UCC records, create a cross-reference list. Look at your credit report for indicators such as open credit accounts, past due payments, or high credit utilization, then align these with your UCC filings. For example, if your Experian report shows an active credit line and your UCC filing shows that line is secured by your receivables, you now understand both the payment behavior and asset risk related to that debt.

Also, use this combined data to spot inconsistencies—for instance, if a loan is marked “closed” on your D&B report but still has an active UCC filing, you’ll know it’s time to contact the lender for a termination. By reviewing both data sets regularly, you’ll maintain a clean and transparent financial profile, reduce your risk of financing denials, and position your business for better lending terms and investor confidence.

u

u