Startups often face the challenge of securing funding, especially in their early stages. Traditional loans, equity financing, and venture capital are common funding options, but they are not always feasible for new businesses. One alternative that has gained popularity in recent years is the Merchant Cash Advance (MCA).

This form of funding is distinct from traditional loans, offering startups a flexible and relatively quick way to access capital. But is it possible for startups to secure funding through an MCA? The answer is yes, but several factors must be considered. This article explores how MCAs work for startups, which startups are most likely to secure one, and why a startup might choose an MCA as a funding source.

While any startup can technically apply for an MCA, those most likely to qualify typically meet certain criteria. Here are some of the key factors that make a startup a strong candidate for an MCA:

Consistent Sales

Startups with consistent daily or monthly sales are better candidates for securing an MCA. Lenders look at the business’s ability to generate steady income as a predictor of future sales. Startups with unpredictable or seasonal revenue may still qualify, but the terms of the MCA may be less favorable.

High Credit Card Sales or Bank Deposits

MCA lenders typically prefer businesses that receive a large portion of their sales through credit cards or bank deposits. This is because they can easily track these transactions and determine the business’s ability to repay the advance. Businesses with high credit card or bank transaction volumes are more likely to secure an MCA because the repayment is directly tied to these transactions.

Established Industry Presence

Startups in industries with proven demand, such as retail, restaurants, and online businesses, are more likely to qualify for an MCA. These industries tend to have predictable cash flow, which gives lenders confidence in the business’s ability to repay the loan. Startups in emerging or niche markets may find it more challenging to secure an MCA due to the higher perceived risk.

Positive Cash Flow

Although MCA lenders are not as focused on credit scores as traditional lenders, they still look at a business’s cash flow to ensure it can repay the advance. Startups with positive cash flow, even if they are in their early stages, are more likely to secure an MCA. Lenders need assurance that the business can generate enough revenue to make daily or weekly payments.

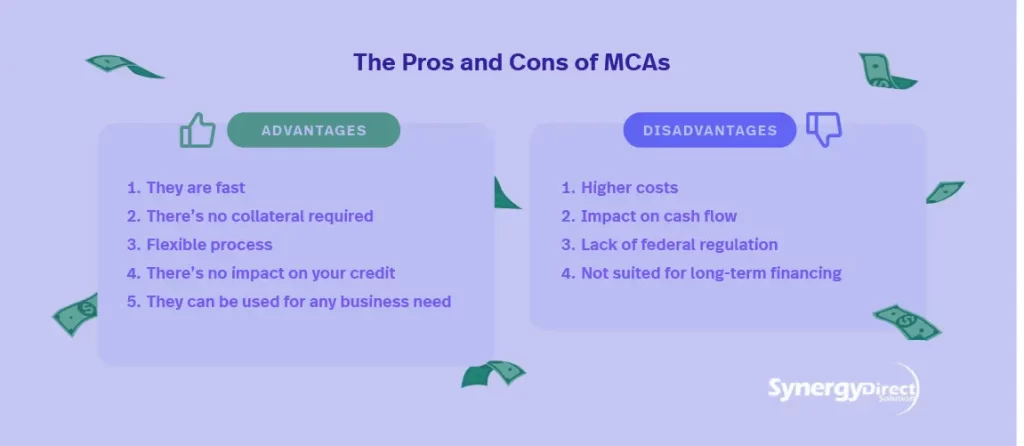

While MCAs can be beneficial for startups, they are not without risks. Here are some of the potential downsides of using an MCA for funding:

High Costs

One of the main disadvantages of an MCA is the high cost of borrowing. MCA lenders typically charge high factor rates, which can make repayment more expensive than traditional loans. In addition, the fees associated with MCAs can be significant, leading to a higher overall repayment amount.

Cash Flow Pressure

Since MCA repayments are tied to daily sales, a startup with fluctuating revenue may face cash flow pressure during slower periods. If a business experiences a downturn, it could struggle to meet repayment obligations, leading to financial strain. This is especially problematic for startups that have unpredictable sales patterns.

Short Repayment Terms

Unlike traditional loans with longer repayment terms, MCAs typically require repayment within a year or less. The short repayment period can put pressure on a startup to generate quick revenue to meet its obligations. If the business doesn’t grow fast enough, it may find itself in a difficult position.

Potential for Debt Cycle

If a startup is unable to meet its repayment terms, it may take out another MCA to cover the existing debt, leading to a cycle of borrowing. This can quickly spiral out of control if the business doesn’t generate enough revenue to repay the advances, causing the startup to fall into a debt trap.

Risk of Over-borrowing

Startups may be tempted to take out an MCA based on their projected sales, but if those projections fall short, they could find themselves over-leveraged. It’s important for startups to carefully assess their ability to repay before taking on this type of financing.